30-Year Treasury Yield Above 5% Signals a Regime Shift

The 30-year Treasury yield above 5% is forcing traders to confront a regime where cheap capital, labor, and energy no longer suppress inflation as reliably.

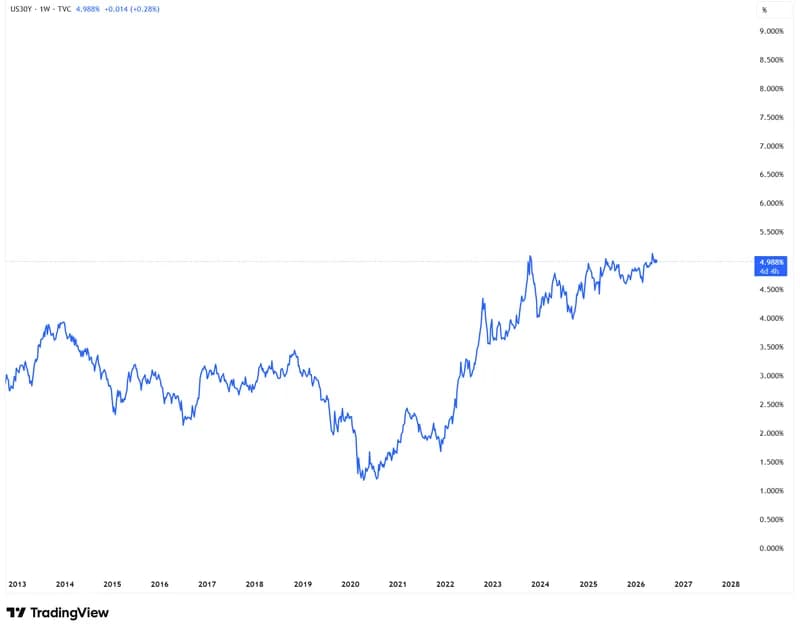

On June 1, 2026, the 30-year Treasury yield had moved back above 5%. The level matters, but the larger signal is more important: traders are starting to accept that the low-rate era may be ending, not merely pausing.

The move is forcing a reassessment of assumptions that shaped markets for decades. Cheap capital, restrained labor costs, and affordable energy helped suppress inflation and support long-duration assets. Each support now looks less dependable. Artificial intelligence adds another uncertainty because it could eventually reduce costs or create a new layer of resource pressure.

The 30-Year Treasury Yield Above 5% Is More Than a Level

The report draws a clear distinction between this move and the brief break above 5% in 2023. Back then, many investors treated the spike as an exception that would reverse. This time, the response suggests that the market is giving more weight to a higher-for-longer regime.

That does not mean every yield move will continue in a straight line. It means the baseline is changing. When the long end of the curve demands more compensation, traders need to examine the conditions behind the move instead of assuming that an old range will automatically reassert itself.

Cheap Capital, Labor, and Energy Built the Old Regime

The 30-year Treasury yield fell from double-digit levels in the early 1980s to roughly 1% during the pandemic. The source argues that this multi-decade decline rested on three forms of cheapness.

Cheap capital came from several directions. Globalization and manufacturing improvements held down goods prices. Oil exporters recycled petrodollars into the United States. Privatized pension systems created demand for financial products. Global investors also accumulated Treasuries because the United States was treated as the safest destination for capital.

Cheap labor reinforced the same pattern. Outsourcing, weaker unions, automation, and a shareholder-first corporate culture restrained wages, especially for workers without college degrees. Lower labor costs helped protect corporate margins.

Cheap energy completed the framework. Dollar-settled global energy trade supported the dollar's international role and helped contain inflation pressure. Together, the three forces gave the United States a long stretch of lower inflation and lower interest rates.

Each Support Is Now Under Pressure

Foroohar's argument is that the old supports are weakening at the same time.

On the capital side, the report points to fewer international buyers at Treasury auctions. Deglobalization and the reshoring of supply chains can raise the price of goods and services in the near term. The petrodollar system is also less secure than it once appeared.

On the energy side, continued tension in the Middle East directly affects energy-importing economies in Asia. The longer-term effect may be more complicated. The source argues that large Asian economies could accelerate clean-energy investment while the United States retreats from climate commitments. That could redirect long-term capital flows toward Asia.

On the labor side, shortages, large strikes, tighter immigration restrictions, and union growth in some white-collar industries have helped push wages higher. Two forces partly offset that trend. Rising employer health-insurance costs can encourage companies to restrain pay, while AI may change the bargaining position of workers in exposed roles.

The key point is not that one pillar has failed completely. Markets are dealing with several pressures at once. A model calibrated to decades of declining yields can miss the combined effect when capital, labor, and energy stop behaving as reliable sources of disinflation.

Debt and Geopolitics Are Raising the Term Premium

The source adds a slower set of variables: rising government debt, intensifying geopolitical friction, and the spread of populism.

These forces matter most at the long end of the curve because lenders are committing capital for years. When the path of inflation, fiscal policy, and political risk becomes harder to price, lenders can demand a higher premium before extending long-term financing. That pressure feeds directly into the 30-year Treasury yield.

This is why the move above 5% cannot be read only as a Federal Reserve story. Short-term policy rates still matter, but long-duration bonds are also reflecting uncertainty about the structure of the economy and the credibility of the old assumptions.

Traders Need to Recalibrate the Baseline

The hardest adjustment is behavioral. Most market participants built their careers during an era when falling rates, restrained inflation, and cheap financing were familiar. Their models and instincts were calibrated to that environment.

Expectation inertia matters. The 2023 move above 5% was easy to dismiss after yields retreated. The current move is harder to treat as a temporary anomaly because several structural supports are shifting together.

The practical takeaway is not to chase a bond-market headline. It is to stop assuming that the previous regime will return on schedule. The 30-year Treasury yield above 5% is a prompt to reassess duration exposure, financing assumptions, and the inflation sensitivity embedded in a portfolio. The next signal will come from whether markets keep demanding a larger premium for long-term capital.

That review should include any position built around cheap refinancing. If the cost of long-term capital stays elevated, a familiar valuation model can produce the wrong answer even when the underlying business has not changed. The rate regime is part of the trade, not background noise.

Worth the read?