What Is a Bid in Trading — Definition and How It Works

A bid is the highest price a buyer will pay for an asset — but understanding how it moves tells you more about market liquidity and positioning than the price itself.

The bid is not a price tag. It is a signal. Most traders treat the bid as a static number — the highest price someone is currently willing to pay for an asset. That understanding is technically correct and practically useless. The real value of the bid is what it tells you about demand, liquidity, and institutional positioning at that moment. When you are trading NQ or ES, the bid reveals who is actually positioned to buy, how much size they are willing to absorb, and whether that demand holds or disappears the instant price moves toward it.

What is a bid in trading

A bid is the highest price a buyer is willing to pay for an asset at any given moment. Every quoted security shows two prices: the bid and the ask. The ask is the lowest price a seller will accept. The gap between them — the spread — is a direct measure of liquidity and a real transaction cost.

The bid sits on the left side of every quote. It represents demand. Whether you are looking at equities, futures, or options, the same structure applies. The bid is where buyers are standing. The ask is where sellers are standing. The market lives in the space between.

How does a bid work in trading

The mechanics are straightforward. When you sell a position using a market order, you fill at the current bid. When you buy with a market order, you fill at the current ask. If you place a limit buy order below the current bid, you wait in the queue until price comes to you — or it does not.

Execution quality depends on understanding where the bid sits relative to your order type:

Market order — fills immediately at the best available bid (selling) or ask (buying). Speed over price control.

Limit order — fills only at your specified price or better. Price control over speed. No fill guarantee.

Stop order — triggers a market order once price reaches your stop level. The fill depends on where the bid or ask is at the moment of trigger, not where you set the stop.

For new traders, a practical checklist: always check the current bid and ask before sending any order. Know the spread. If the spread is unusually wide, a market order can cost you more than expected. If you can wait, a limit order gives you control over fill price.

Bid vs. ask — what is the difference

The bid and ask are two sides of the same transaction. The bid represents buyers. The ask represents sellers. The spread between them is not arbitrary — it reflects the cost of immediacy and the depth of participation in that market.

A stock like AAPL might show a bid of $195.00 and an ask of $195.02 — a two-cent spread that reflects deep liquidity and heavy competition between buyers and sellers. An ETF with lower volume during extended hours might show a $0.15 or $0.25 spread. Futures contracts like NQ typically have tight spreads during regular trading hours but can widen meaningfully during overnight sessions or around major economic releases.

Tight spreads signal liquidity. Wide spreads signal the opposite. Every market order you send pays the spread as an implicit cost.

Bid example — reading a live quote

Suppose stock XYZ is quoted at a bid of $50.00 and an ask of $50.05.

If you own XYZ and want to sell immediately, you fill at $50.00 — the bid.

If you want to buy XYZ immediately, you fill at $50.05 — the ask.

The spread is $0.05. That is your cost of instant execution.

On highly liquid names, that spread might be a single penny. On less liquid securities, it can be significantly wider. The size of the spread tells you how much it costs to get in and out without waiting.

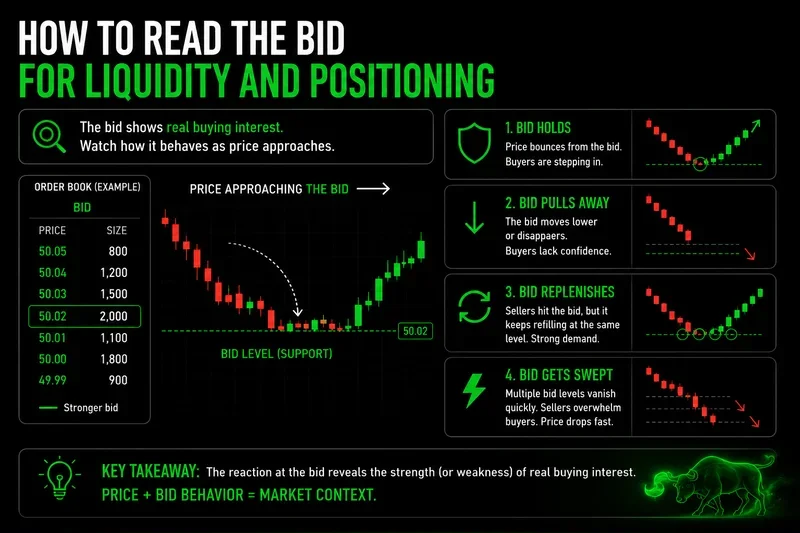

How to read the bid for liquidity and positioning

This is where the bid stops being a simple price reference and becomes a diagnostic tool.

In deep, liquid markets with institutional participation, the visible bid reflects real positioning. It is not just a number — it represents actual orders from actual capital. Watching how the bid behaves as price approaches it tells you about market structure and real-time demand:

Bid holds under selling pressure — genuine buying interest. The level has real depth behind it.

Bid gets pulled before price arrives — the orders were either strategic or spoofed. The apparent demand was never real.

Bid size increases as price approaches — more buyers stepping in. Demand is building.

Bid thins out after a test — the level has been weakened. Fewer participants are willing to defend it.

This behavior is the difference between a price level that means something and one that is just a number on a screen. The durability of the bid under pressure reveals the depth behind it.

Common bid mistakes beginners make

The bid looks simple. The mistakes that come from misunderstanding it are expensive.

Ignoring the spread on a market order. A tight-looking spread can widen in milliseconds. What looked like a clean entry can cost more than expected once the order hits the book.

Chasing the bid higher. Price is moving up, you pull your limit order higher to catch it, and you fill at a worse level than if you had waited. Chasing the bid is emotional execution, not disciplined entry.

Canceling when price approaches your order. Fear of a fill is a discipline problem. If the setup is valid and the risk is defined, let the order work. Canceling at the last second and watching the move happen without you is a pattern that compounds.

Confusing the bid with the last traded price. The bid is where the next buyer stands. The last price is where the last trade happened. They can be the same, but they often are not — especially in fast markets.

When the bid framework breaks down

The bid is a reliable signal in liquid, actively traded markets with genuine institutional participation. In those conditions, it reflects real positioning and real depth.

This framework inverts in thin conditions. During overnight sessions in low-volume futures, pre-market gaps, or the moments before major economic releases, the visible bid can disappear instantly. Market makers pull their quotes. What looked like a solid floor was never real demand — it was resting orders waiting to be removed. In those environments, the bid is a snapshot of intent that can change faster than you can react. Trading based on bid behavior in those conditions is a different skill set, and one that requires significantly more caution.

FAQs

What is a bid in simple terms? A bid is the highest price a buyer is currently willing to pay for an asset. It sits on the left side of every quote, opposite the ask, which is the lowest price a seller will accept.

What is the difference between a bid and an ask? The bid is what buyers offer. The ask is what sellers want. The spread between them reflects liquidity and is an implicit transaction cost for anyone executing at market.

Can you buy at the bid price? Yes — if you place a resting limit buy order at the bid and a seller hits it, you fill at that price. A market buy order, however, fills at the ask.

Why do bid-ask spreads matter? Tight spreads indicate high liquidity and low transaction costs. Wide spreads mean less participation and higher costs to enter or exit a position. Every market order pays the spread.

Worth the read?